NBA Moneyline Betting for UK Punters

The first NBA bet I ever placed in the UK was a moneyline on a Tuesday-night Lakers game, and I almost talked myself out of it because the price looked…

Apply the Kelly criterion to your NBA bets. Compare odds at UK sportsbooks, size your wagers perfectly to maximize ROI, and grab exclusive promo bonuses.

Table of Contents

The first time I tried full Kelly on NBA bets, I went bust on a £500 starting bankroll inside six weeks. The maths was correct. My estimate of my edge was not. That experience is the one I open with whenever I talk to UK punters about Kelly, because the formula is famous for the right reasons and dangerous for the wrong ones. Used carefully, it sizes your bets in proportion to your edge. Used carelessly, it bankrupts you faster than flat staking ever could.

The Kelly Criterion is a stake-sizing formula developed by John Kelly Jr. at Bell Labs in 1956. Originally written for signal-to-noise problems in telecoms, it was adapted by gamblers in the 1960s and 1970s and has since become the canonical answer to the question “how much of my bankroll should I bet?”. The maths is elegant: stake a fraction of your bankroll equal to your edge divided by the odds offered. The complication is that estimating your edge accurately is the hard part of NBA betting, and Kelly punishes overestimation severely.

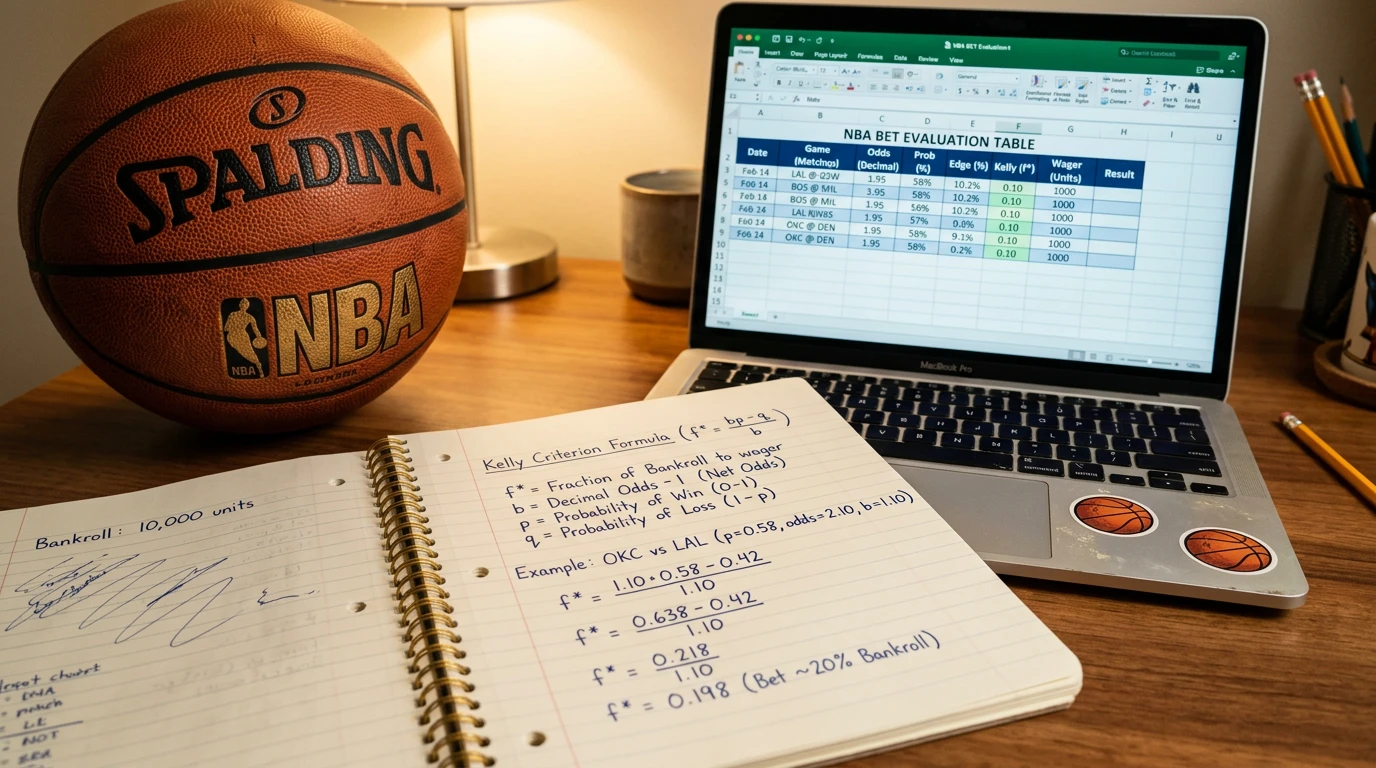

The formula for a two-way market like an NBA moneyline, spread, or total is:

f = (bp - q) / b

Where f is the fraction of your bankroll to stake, p is your estimated probability of winning, q is 1 minus p (the probability of losing), and b is the decimal odds minus 1 (your net winnings per unit staked if you win).

Walk through a real example. Suppose you’ve taken a moneyline on the Bucks at decimal 2.10, which is +110 in American or 11/10 fractional. Your model says the Bucks win 52% of the time. Plug the numbers in: b = 1.10, p = 0.52, q = 0.48. f = (1.10 × 0.52 - 0.48) / 1.10 = (0.572 - 0.48) / 1.10 = 0.092 / 1.10 = 0.0836. So full Kelly says stake 8.36% of your bankroll on this bet. On a £1,000 bankroll, that’s £83.60.

The intuition behind the formula is that the larger your edge, the more you should stake. The smaller your edge, the less you should stake. If your estimated probability exactly matches the bookmaker’s implied probability – meaning no edge – Kelly returns zero. You don’t bet. If your edge is negative – meaning you think the bet is worse than the implied price – Kelly returns a negative number, which means you should bet the other side.

The catch, which is the catch with all Kelly applications, is that p is your estimate of the true probability. Your estimate could be wrong. If you say p = 0.52 but the true probability is actually 0.49, you have negative edge and Kelly is recommending you stake at the wrong size on the wrong side. The formula is only as accurate as your probability estimate.

Here’s the thing – almost nobody serious uses full Kelly. The standard practice across the professional NBA betting community is fractional Kelly, typically half Kelly or quarter Kelly. Why? Because full Kelly maximises long-term geometric growth, but the path to that growth is so volatile that most humans can’t hold their nerve through the drawdowns.

The drawdown profile of full Kelly is brutal. If your model has even moderate noise in its probability estimates, you’ll face stretches where you lose 30% to 50% of your bankroll across a few weeks of bad variance, even though your long-run edge is intact. That’s a real bankroll going to half its starting size, and the typical UK punter pulls the cord, withdraws what’s left, and never trusts the system again. Half Kelly cuts the volatility roughly in half while preserving about 75% of the long-run growth. Quarter Kelly cuts it further at the cost of more growth. Most successful long-term bettors I’ve spoken to run somewhere between quarter Kelly and half Kelly.

There’s also the model-uncertainty argument. If you genuinely knew the true probability of every NBA market, full Kelly would be optimal. You don’t. Your probability estimates have an error band around them. Fractional Kelly is the mathematically honest response to that uncertainty – you’re shrinking your stake toward the no-edge level to account for the chance your edge isn’t as big as you think.

Practical implementation: pick your fraction at the start and stick to it. Don’t move from quarter Kelly to half Kelly because you feel confident this week. Don’t move from half to full because you’ve just hit a hot streak. The discipline matters more than the precise fraction. UK demographics for sports betting show 16% of men versus 4% of women placed bets in April to July 2025 across all online sports markets, and survey data suggests the men in that pool tend to overestimate their edge – exactly the population most likely to lose money sizing too aggressively.

Kelly was developed for sequential independent bets. NBA betting routinely involves correlated bets – multiple legs in a same-game parlay, multiple positions across the same fixture, simultaneous bets on related markets. The formula doesn’t translate cleanly to those situations.

The naive approach is to compute Kelly for each leg independently and stake accordingly. That over-allocates capital because the legs aren’t independent. If you’ve staked Kelly-sized positions on the spread, the total, and a star player’s points all in the same game, you’re effectively staking a much larger fraction of your bankroll on the underlying outcome than Kelly intended.

The correct treatment is to estimate the joint probability of the combined outcome and apply Kelly to the combined bet. For an SGP at the bookmaker’s quoted price, that means computing your own estimate of the joint probability and using the SGP price as the offered odds. If your joint probability estimate is higher than the bookmaker’s implied joint probability, you have edge and Kelly tells you the stake. If it’s lower, you don’t bet.

This is harder than it sounds, because estimating joint probabilities for correlated legs requires assumptions about the correlation structure, and small errors in those assumptions get amplified in the final probability estimate. The practical UK answer is to avoid sizing SGPs with Kelly unless you have a tested model. Use a flat fraction of your bankroll – say 0.5% to 1% – for SGP recreational play, and reserve Kelly sizing for single-leg bets where the model risk is more manageable.

Three failure modes show up over and over in UK punters trying Kelly. They’re worth naming.

The first is overestimating your edge. Most punters’ subjective probability estimates are systematically too confident. If you think the Bucks win 52% of a game where the market implies 50%, your estimate has about a 60% chance of being closer to the market than to your read. Kelly applied to optimistic probabilities is mathematically destructive. Half Kelly partially insulates against this; quarter Kelly more so.

The second is recalculating your bankroll after every bet. If you start with £1,000 and win £80 on Tuesday, then bet half Kelly on a Wednesday game at the new bankroll of £1,080, you’re slowly increasing your absolute stake even though your edge per bet hasn’t grown. The conservative practice is to set a fixed bankroll at the start of a period – say, a month – and use that as the Kelly denominator until the period ends. Recalculating mid-period leads to ratchet-up behaviour after winning streaks and ratchet-down panic after losing streaks.

The third is mixing bet sizes across different conviction levels. A 3% edge bet and a 1% edge bet are both Kelly-positive, but sizing them identically wastes the formula’s advantage. The whole point of Kelly is that bigger edges get bigger stakes. If you’re not differentiating, you might as well flat-stake – which is sometimes a perfectly reasonable choice, and the comparison between Kelly and flat unit sizing is worth working through in detail. The compare Kelly with flat unit sizing piece walks through both approaches with NBA-specific examples.